聚合智慧 | 升华财富

聚合智慧 | 升华财富

产业智库服务平台

产业智库服务平台

|

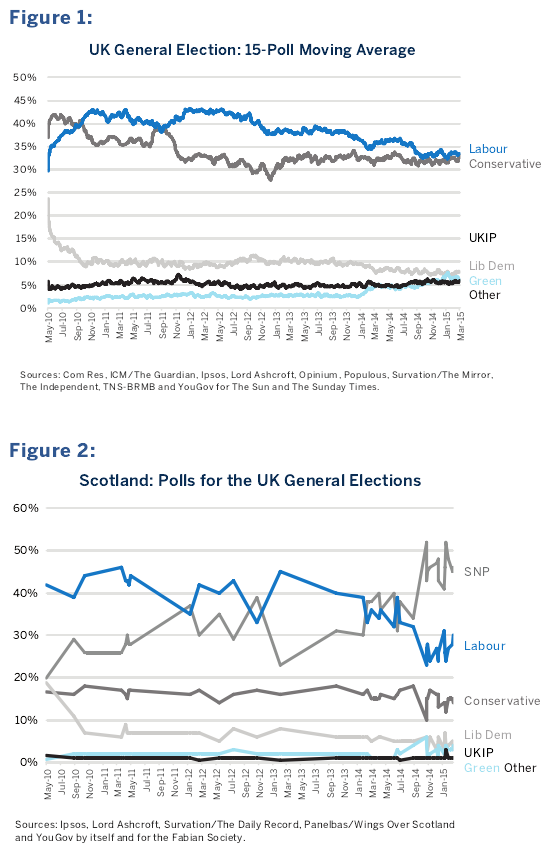

UK Elections, European Disunion and Financial Markets All examples in this report are hypothetical interpretations of situations and are used for explanation purposes only. The views in this report reflect solely those of the authors and not necessarily those of CME Group or its affiliated institutions. This report and the information herein should not be considered investment advice or the results of actual market experience. On May 7, 2015, the United Kingdom will hold elections that could dramatically reshape its relationship with the European union (EU). Currency patterns for both the Pound and Euro might be disrupted as trading relationships could be thrown into doubt. To examine the contours of the political landscape, we will start with the two major parties, although, the eventual election outcome might be determined by the growing strength of Britain’s smaller parties. Labour Party, which last ran the country from 1997 to 2010, generally takes a pro-European stance. Gordon Brown, who served as Chancellor of the Exchequer under then Prime Minister Tony Blair from 1997 to 2007 prior to becoming Prime Minister himself, aspired to have the UK join the Euro. Blair himself attempted, unsuccessfully, to become President of the European Commission after leaving office. Labour’s approach to the EU is to negotiate on behalf of UK interests within the European framework, and the party is generally more favorable to European integration. Labour’s position on the EU is rather straight forward compared to that of its main rival, the Conservative Party. The Conservative Party (Tories) has a more complicated relationship with the EU. The party has long been split between a dominant pro-European faction and a smaller but vocal Eurosceptic wing. Margaret Thatcher, who identified closely with the Eurosceptics, was ousted as Prime Minister in 1990, in part, because of her opposition to joining the Exchange Rate Mechanism that eventually converged the various European currencies into the Euro. Although her successors, including Prime Ministers John Major and David Cameron, were more pro-European, the leader of the Conservative Party has to spend considerable time managing the Eurosceptics. Recently, this task has been complicated by the rise of the UK Independence Party (UKIP), which has siphoned off more voters from the Tories than from other UK parties. As such, Cameron has promised that if voters return his party to office in 2015, he will call for a non-binding referendum on the EU. If the referendum takes place, it is entirely possible that UK voters would voice their opinion that it is time to leave. Additionally, the Conservatives favor softening financial regulations proposed by the Brussels-based EU which they see as a threat to London’s financial services industry. The UK’s other parties add complexity. UKIP, of course, opposes continued membership in the EU. The party used to be fairly marginal, garnering just 3.1% of the vote in the 2010 elections, but since then its ranks have swelled. In 2014, UKIP took 27.5% of the vote in UK’s European parliamentary elections, pushing Cameron’s Conservatives into a humiliating third place. Currently, they are running around 15% (Figure 1) in the polls for the upcoming UK Parliamentary elections – not enough to win many seats but possibly enough to undermine the Tories’ chances of winning outright. The Liberal Democrats (Lib Dems), by contrast, are ardently pro-European. Currently, they govern with the Conservatives as the junior member of the coalition government. For their part, the Lib Dems have collapsed in the polls (to around 7% from 23% in the 2010 elections (Figure 1)) and look set to lose most of their representation in Parliament. This makes it very unlikely, though not impossible, that they will remain in government after May 2015. Lib Dem leader and Deputy Prime Minister Nick Clegg even warned that one-party Tory rule would lead to the break-up of the UK, stating, “As night follows day, if the UK falls out of the European Union, Scotland, in my view, within a heartbeat, will pull out of the UK. We will then have lost two unions in one parliament.”

Finally, there is the Scottish National Party (SNP). The SNP is best known for losing the independence referendum in September 2014. Do not be fooled -- if the polls are to be believed, they appear to be on the verge of wiping out Labour in Scotland (Figure 2). Before the referendum vote, Cameron promised the Scottish people devolution –more local control over their governance. Scottish voters might hold him accountable by electing more SNP members of parliament (MPs), and if so, it will not come at the Tories’ expense because they have only one seat left in Scotland. Rather, it will come exclusively at the expense of Labour’s 41 Scottish seats. If current polls hold, Labour stands to lose approximately half of its Scottish representation –precious seats it will need to retain if it is to secure a majority in Westminster. A SNP rout may deny Labour a majority in Parliament in Westminster even if Labour out- performs the Tories in the popular vote country-wide. For the moment, the elections appear as though they will be closely contested and it is difficult to privilege one outcome over another. That said, we see three major scenarios as worth examining: 1) Tory Win 2) Hung Parliament 3) Labour Win These three scenarios could produce significantly different outcomes with respect to the UK’s relationship with the European Union. Let’s explore them one by one. Scenario 1: Outright Tory Win This scenario is not as farfetched as it might sound. While the Conservatives have been behind in the polls nearly 100% of the time since the current Tory-Liberal Democrat coalition took office in May 2010, they have a long history of outperforming opinion polls on Election Day. One might also say that the Labour Party has a long history of snatching defeat from the jaws of victory. Either way, Prime Minister Cameron’s Conservatives could win; they have been catching up in the polls. As previously noted, Cameron has promised that if his Conservative Party wins, he will call for a non-binding referendum as to whether the UK should remain a part of the EU. Moreover, public opinion polls indicate that if such a referendum was held, the UK public would vote in favor of leaving the EU. As such, a Tory win could move markets, possibly putting pressure on UK equities and the Pound while supporting UK fixed income in the short to intermediate term. The Euro relative to the US dollar might also be destabilized. There is considerable debate over the consequences of the UK leaving the EU. Some consider that it would be a disaster for British businesses and the economy, and would reduce the UK’s influence in Europe. However, others argue that if the UK were to leave, it might not be such a big deal. They point out that the UK could work out an agreement with the EU that resembles the one that Norway and Switzerland have with the group. Although neither Norway nor Switzerland are members of the EU, their citizens move freely within the EU – in fact, more freely than UK citizens currently do. Moreover, Norwegian and Swiss businesses are deeply integrated with their EU counterparts. Finally, as the Swiss have discovered, not having joined the EU does not exempt Swiss financial institutions from the reach of regulators and tax authorities across the continent. UK citizens, banks and other businesses might find themselves in the same boat were they to leave the EU, depending upon what sort of agreement was reached and how disruptive a transition out of the EU would be. It is also worth noting that the UK, like non-EU members Norway and Switzerland, remained outside of the common currency. Scenario 2: Hung Parliament By its very nature, this is the most difficult scenario to evaluate because it would depend on how the seats in Parliament are divided among the smaller parties. If it is another Conservative-Lib Dem government, Cameron will likely have to call a referendum regarding EU membership. The outcome would likely resemble Scenario 1, but the Lib Dem’s are not likely to want to be a part of another coalition. As has been observed in many countries, the smaller party in a coalition government often loses popularity substantially at the next election. If a hung Parliament produces a Labour-Lib Dem or a Labour-SNP government, the outcome would be considerably more pro-European and a referendum would be unlikely during the term of office of any such coalition. The present coalition aside, hung Parliaments have often proved to be short-lived. The one formed in February 1974 did not make it past October of the same year. The Lib-Dems insisted on a full fixed-term parliament as the price for being part of the current coalition with the Tories. The idea of a full fixed-term Parliament may be losing its appeal. In any case, a Labour-based coalition might also spell market volatility even if the UK-EU relationship is maintained, given the policy uncertainties that would accompany such a government. Scenario 3: A Labour Victory This is the scenario favored by public opinion polls until recently. The chances of an outright Labour majority, however, appear to be diminishing. If Labour comes to power, it is unlikely that it will call a referendum on EU membership. The UK will continue to have plenty of bones to pick with the EU over matters like financial services regulation but any such dispute would likely be handled within the usual EU framework. This scenario would likely have UK equities breathe a sigh of relief in the short run but might be of little consequence in the long-run. The UK has often had an uneasy relationship with the EU. In 1967, French President Charles de Gaulle said “non” to the UK joining the European Economic Community (EEC), the EU’s predecessor. Even after the UK joined the EEC in 1973, relations with its European partners were not always smooth. During the 1980s, some of Thatcher’s most famous one-liners had to do with disputes between the UK and the European Community, including her famous “I want my money back” remark (referring to agricultural subsidies) and her “No, no, no” speech to Parliament (regarding the efforts to expand the EU’s powers into health care policy, national security, and the creation of a common currency). Things have not gotten easier over the past quarter century, most especially, since the financial crisis. The UK is at a fork in the road with respect to Europe. Whichever path voters choose, it will have plenty of short-term consequences for financial markets. How much a decision to leave the EU matters in the long run is a subject of considerable debate that will intensify ahead of a referendum, should one occur. For centuries, the UK’s overriding foreign policy goal has been to make sure that no one power comes to dominate the continent (see Spain in the 1500s and early 1600s, France in the late 1600s up to the 1870s, Germany from 1870 to 1945 followed by the Soviet union until 1991). If the UK leaves the EU, it will lose its direct leverage over decision-making in Brussels but could still pursue its divide-and-conquer strategy by setting the remaining EU members against one another on issues of interest to the UK, including financial services regulation, while still cooperating with the EU and its member states in other areas such as national security and intelligence. The EU, however, could do the same, pitting Scotland against England within the UK. Interesting times ahead! 文中显示的任何交易代码仅作为演示计,并不代表推荐意图。 盈透交易员睿智中提供的内容(包括文章和评论)仅作为资讯用途。发布的内容并不代表盈透证券建议您或您的客户联系独立顾问或对冲基金以期获取其服务或投资其产品,也不代表建议您联系在盈透交易员睿智发布文章或向顾问、对冲基金投资的相关人士。在盈透交易员睿智中发布文章的顾问、对冲基金或其他分析师均独立于盈透证券,盈透证券不会对这些顾问、对冲基金或其他人士的过往或将来表现,或其提供的信息之准确性做出任何声明或担保。盈透证券不会进行“适宜性评估”来确保顾问、对冲基金或其他参与方的交易适合于您。 发布内容中提及的证券或其他金融产品并非适合所有投资者。发布的内容并未从您的投资目标、财务状况或需求出发,并不旨在向您推荐任何证券、金融产品或策略。进行投资或交易前,您应考虑该产品是否适合您的特定情况,如有需要,请咨询相关人士获取专业的建议。过往业绩并不代表将来表现。 盈透或其分支机构的雇员所发布的任何信息均基于公认的真实可信的信息。然而,盈透或其分支机构无法保证信息的完整性、准确性和适当性。盈透不对任何金融产品其过去或将来的表现作出任何声明或担保。交易员睿智中发布的文章并不代表盈透认为任何特定金融产品或交易策略适合您。 The analysis in this article is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IB to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

★美国盈透证券是全美营收交易量最大的 顶尖互联网混业券商 盈透证券集团(IBG LLC)拥有超过50亿美元的综合股本资产 ★单一账户 多币种 直接接入全球24个国家100+市场中心,实现股票、期权、期货、外汇、债券、ETF及价差合约的全球配置 ★美国盈透证券有限公司的客户证券账户受到证券投资人保护公司("SIPC")最高达50万美元(现金额度25万美元)的保护 ★超低手续费 不卖订单流 致力提供最佳执行价格 ●享受盈透低佣金 外盘开户请点击: https://www.ibkr.com.cn/mkt/?src=7h5&url=%2Finv%2Fcn%2Fmain.php%23open-account ●详细开户流程: http://www.7hcn.com/article/187153-1.html 美国期货及期货期权收费根据交易量阶梯式计算 盈透佣金0.25-0.85美元/手 美股佣金半美分/股 超低隔夜融资利息 1000万美元年化利息低至0.594% (按目前基准利率0.13%计算)

每股净美元改善定义: ((价格改善股票数目 * 价格改善数额) - (没有价格改善股票数目 * 没有改善数额)) = 总执行股票数目 交易审计集团(TAG)。根据TAG,比较期间行业 作为整体考虑。TAG关于美国股票的分析包括所有100股或上至10,000股的市场定单。美国期权的分析包括所有市场定单尺寸并包括基于IB的成本相加 定价结构的客户收到的交易所回扣。 TAG对传递到欧洲交易所的定单的分析包括在正常交易时段内的所有传递执行的定单,包括交易所上市的股票的所有市价单和可交易的限价单以及近于市价单的定 单(定单收到时的限价价格距报价在十分之一欧元以内),并按每个交易所的执行交易量加权计算。欧洲股票的交易所包括XETRA, EURONEXT, CHI-X, WIENER BORSE, TURQUOISE,LONDON以及NASDAQ OMX。 ★专业交易平台- 交易者工作站(TWS)、网络交易者及多种移动交易端选择,包括手机交易平台及iPad交易平台方便您随时随地把握市场走势并及时作出交易指令, 并提供API及FIX连接解决方案 ★投资人服务商市场 向财务顾问、基金经理及第三方服务商提供向全球投资人展示业绩并开展合作的免费平台 ★根据不同客户需求 支持多种账户类型 包括对冲基金、职业/非职业顾问、自营交易商及白标经纪商账户 根据巴伦周刊互联网券商评比,盈透证券从2002年至2016年连续15年被巴伦周刊(Barron's)评为低成本经纪商:2002 - 5星,2003 - 4.9星,2004 - 5星,2005 - 5星,2006 - 5星,2007 - 4.8星,2008 - 4.5星,2009 - 4.5星,2010 - 4.2星,2011 - 4.5星,2012 - 4.3星,2013 - 4.5星,2014 - 4.5星,2015 - 4.5星,2016 - 4.5星。在巴伦周刊(Barron's)2016年3月21日的年度最佳互联网券商评比 - “网络投资者的最大顾虑?移动安全”中,盈透证券荣获4.5星评级。评比的条件包括交易体验和技术,使用性,移动性,交易产品范围,研究手段,投资组合分析和报告,客户服务和教育,以及成本。Barron's是Dow Jones & Co. Inc的注册商标。

欲了解更多信息请关注美国盈透证券公众微信号 或登录美国盈透证券官方网站:www.ibkr.com.cn/7hcn 欲了解更多信息请美国盈透证券官方网站:www.ibkr.com.cn 或直接联系我们深入了解个人账户及机构账户的相关服务: +852 2156 7907 ●享受盈透低佣金 外盘开户请点击: https://www.ibkr.com.cn/mkt/?src=7h5&url=%2Finv%2Fcn%2Fmain.php%23open-account ●详细开户流程: http://www.7hcn.com/article/187153-1.html

责任编辑:叶晓丹 |

【免责声明】本文仅代表作者本人观点,与本网站无关。本网站对文中陈述、观点判断保持中立,不对所包含内容的准确性、可靠性或完整性提供任何明示或暗示的保证。请读者仅作参考,并请自行承担全部责任。

本网站凡是注明“来源:七禾网”的文章均为七禾网 www.7hcn.com版权所有,相关网站或媒体若要转载须经七禾网同意0571-88212938,并注明出处。若本网站相关内容涉及到其他媒体或公司的版权,请联系0571-88212938,我们将及时调整或删除。

首页广告.png)

七禾研究中心负责人:刘健伟/翁建平

电话:0571-88212938

Email:57124514@qq.com

七禾科技中心负责人:李贺/相升澳

电话:15068166275

Email:1573338006@qq.com

七禾产业中心负责人:果圆/王婷

电话:18258198313

七禾研究员:唐正璐/李烨

电话:0571-88212938

Email:7hcn@163.com

七禾财富管理中心

电话:13732204374(微信同号)

电话:18657157586(微信同号)

七禾网 |  沈良宏观 |  七禾调研 |  价值投资君 |  七禾网APP安卓&鸿蒙 |  七禾网APP苹果 |  七禾网投顾平台 |  傅海棠自媒体 |  沈良自媒体 |

© 七禾网 浙ICP备09012462号-1 浙公网安备 33010802010119号 增值电信业务经营许可证[浙B2-20110481] 广播电视节目制作经营许可证[浙字第05637号]