聚合智慧 | 升华财富

聚合智慧 | 升华财富

产业智库服务平台

产业智库服务平台

|

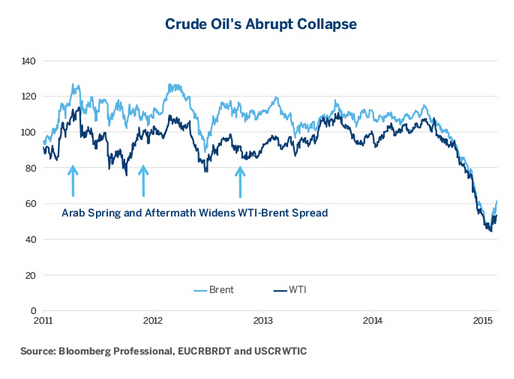

The Geopolitical and Economic Consequences of Lower Oil Prices Since June 30, 2014, crude oil prices have been nearly halved (Figure 1). Still, the direction of oil prices is uncertain and there is a very real possibility that they may remain low for several years. Despite advances in alternative fuels and efforts at conservation, oil remains the life blood of the world economy and essentially the only meaningful transportation fuel. As such, lower oil prices will have enormous economic and political consequences that will be felt globally in a variety of ways. Figure 1.

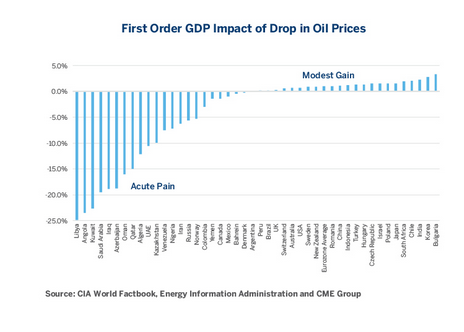

Modest Gain versus Acute Pain For oil consumers, lower prices are akin to a tax cut. This will allow them to do a combination of the following: increase savings, pay down debt and increase consumption. In most countries, consumers will gravitate towards spending more. The biggest beneficiaries will be the countries with no significant oil resources of their own, such as the nations of Eastern Europe, and some Asian economies, including India, South Korea and Japan. For the most part, the gains to be had from lower oil prices are fairly modest and in the order of 0%-2% of GDP and never higher than about 3% (Figure 2). Figure 2.

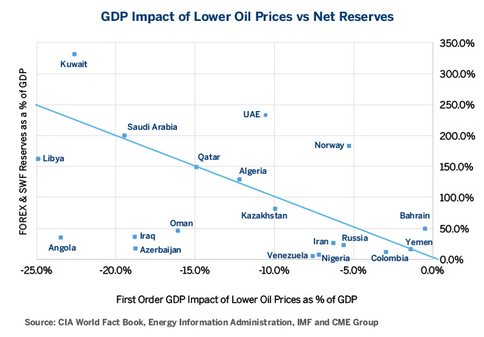

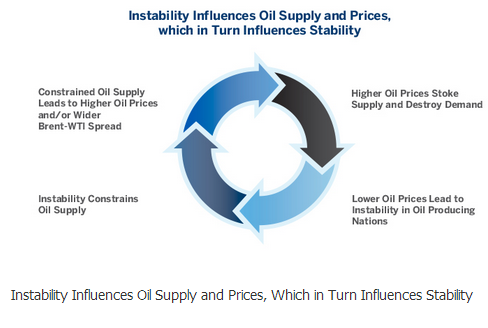

Since oil production is heavily concentrated in only about two dozen countries, some of these nations will feel the pain of lower oil prices acutely, with the first order GDP impact as large as -10% to -25% (Figure 2). (When looking at Figure 2, please bear in mind that the countries where the drop in oil prices will have a negative first order impact on GDP account for only 14% of world GDP, whereas the beneficiaries make up the remaining 86% of world output). Among oil producers, the impact will vary greatly from one country to another, depending upon three factors: The proportion of oil production that is exported versus consumed domestically. The size and diversity of the country’s economy. The amount of foreign exchange and other reserves available to meet the country’s needs. Some major oil producers such as China, the United Kingdom and the United States will actually be net beneficiaries of the decline in oil prices since they consume more than they produce. Others will take a serious hit to their GDP but the impact will be cushioned by their large foreign exchange reserves and sovereign wealth funds (SWFs). These nations include many of the Persian Gulf states such as Saudi Arabia, Kuwait, Qatar and the United Arab Emirates, as well as Algeria and Norway (Figure 3). By contrast, net oil exporters who are the most vulnerable from protracted low prices include Angola, Azerbaijan, Colombia, Iran, Iraq, Kazakhstan, Libya, Nigeria, Oman, Russia, Venezuela and Yemen. Their foreign exchange reserves and SWF assets are fairly small relative to both their economic output (less than 50% of GDP) and the negative impact of lower oil prices (Figure 3). As such, these nations have the greatest potential for instability. In some cases, instability in those nations could lead to a reduction of oil production (Figure 4), which in turn could push crude oil prices higher or cause the spread between Brent and WTI to widen, as was the case when the Gaddafi regime collapsed in 2011, throwing Libya into chaos. The economic impact will be very different in countries such as Colombia and Russia, which have free floating currencies, rather than in nations with less flexible exchange rate regimes. Countries with a floating exchange rate have a choice between imposing very high interest rates to keep their currencies stable or letting their currencies fall and suffer through higher inflation rather than necessarily a deeper hit to the economy. Figure 3.

Figure 4.

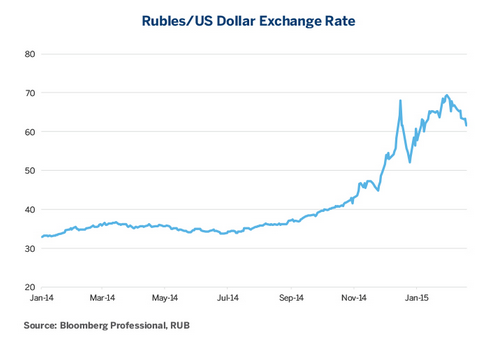

Here is our summary of the key benefits of lower oil prices and how they are likely to play out in each region/country: 1.Central Europe: Aside from Romania, Central Europe produces almost none of its own oil. Moreover, since these countries are on the lower end of Europe’s income scale, they spend a higher percentage of GDP on imported oil than their Western European peers. Bulgaria may be the biggest beneficiary with a gain of as much as 3% of GDP but the Czech Republic, Hungary, Poland and Romania could get a 1.0-1.5% GDP boost. 2.Eurozone Europe: The countries that share a common currency produce barely a drop of their own crude oil. As such, they are likely to benefit from the drop in oil prices. As a first order GDP impact, Italy will gain 0.9%, France and Germany about 1.0%, and Spain as much as 1.5%. Greece may be the biggest winner (whether it stays in the Eurozone or not) with a gain of 2.2% of GDP. The actual GDP impact, however, could be much smaller. If Europeans come to expect deflation, they may choose to save the money that they technically no longer have to spend on petrol rather than on other items. Moreover, since petrol is heavily taxed in most of Western Europe, the impact on consumers will be more modest than it might otherwise be. The impact of these high taxes is evident in the relatively low level of per person petrol consumption, which is about half that of US levels. 3.South Korea and Japan: Like Eurozone nations, South Korea and Japan produce essentially none of their own petroleum. Japan may benefit from lower oil prices to the tune of 1.5% of GDP as a first order effect, while South Korea may get a boost of 2.8%. In Japan, it should be noted however, that lower oil prices may translate into higher saving rates rather than greater consumer spending if the Bank of Japan’s quantitative easing program fails to send inflation expectations higher. On another note, since Japan shut down most of its nuclear facilities in the aftermath of the Fukushima incident, lower oil prices will also reduce the country’s trade deficit through cheaper energy imports. 4.India: Should get a boost of about 2.2% of GDP from lower oil prices. There will be little in any consumer benefits, however, as cheaper oil simply means that the government will spend less in fuel subsidies. Thus, the main benefit of lower oil prices will be a smaller fiscal deficit. This may allow Narendra Modi’s government some wiggle room in implementing potentially controversial reforms that have been delayed since he took office last spring. Already his government is proposing to increase transfers to India’s regional governments to pave the way for acceptance of reforms that the central government advocates. 5.China, the UK and the USA: These countries meet some of their domestic petroleum needs from their own production. The UK will be smallest beneficiary with a first order GDP gain of 0.3%, followed by 0.7% for the US and 1.1% for China. In the UK, gains to consumers will be blunted by a very high domestic fuel tax and by potential declines in North Sea oil investment and maintenance. Likewise, while US consumers will benefit from lower prices, US oil producers are already cutting back considerably on exploration and investment. Lower oil prices will be bad for states like Alaska, North Dakota, Oklahoma, and Texas but good for almost everyone else. 6.Other beneficiaries: Most countries aren’t oil producers. As such, nations as diverse as Australia, Chile, Israel, New Zealand, Turkey and most emerging countries of Asia and Africa will also be net beneficiaries of lower oil prices, with GDP impacts in the 0.5%-3.0% range, with the poorer nations benefitting disproportionately. So now onto who gets hurt, how badly and the potential consequences: Algeria: Lower oil prices could cut nearly one eighth (12.2% by our calculation) off Algeria’s GDP if they don’t rebound. Algeria has been remarkably stable in recent years. After a civil war from 1991 to 2002 that claimed over 60,000 lives, Algeria managed to avoid the tumult of the Arab Spring that swept away governments in neighboring Libya and Tunisia. The good news is that the country used the boom times in the petroleum industry to amass considerable currency reserves of $192 billion as well as stash an additional $77 billion in a SWF called the Revenue Regulation Fund. These funds total almost 130% of annual GDP and should provide the Algerian economy and government some cushion against the impact of lower oil prices. Even so, given the instability on Algeria’s eastern border with Libya, the potential for increased security problems cannot be ignored. Angola: The boom in oil briefly made Angola’s capital Luanda one of the most expensive cities in the world, but also brought economic growth and prosperity to at least parts of a country that spent most of its post-independence period mired in civil war and poverty. As such, it can’t be welcome news that the decline in oil prices shaved an estimated 23% from the country’s GDP, the second hardest hit in the world. Moreover, Angola hasn’t built up currency reserves or SWF funds that compare to those of the Gulf states, leaving it in a comparatively vulnerable position in the face of reduced oil revenues. This may diminish the ability of the Angolan government and Sonangol, the Angolan oil company which is deeply intertwined with the state, to fund infrastructure improvements, offshore oil investments and to keep a potentially restive population appeased. Azerbaijan: Russia isn’t the only former Soviet Republic to suffer when oil prices decline. Azerbaijan appears likely to take a far bigger hit than its northern neighbor, with lower oil prices shaving off as much as 18% of GDP. Unfortunately for the Azeri’s, they aren’t buffered by a SWF and their currency reserves amount to only about 18% of GDP, providing very little cushion. For the moment, it’s not clear how the collapse in oil prices will impact Azerbaijan in its relationship with Armenia, with whom it fought over the breakaway Nagorno-Karabakh region in the early 1990s, or with Russia, which is a close ally of Armenia. Russia’s position in the region has been weakened by it loss of influence over Ukraine’s government in 2014 as well as by the collapse in oil prices that also hampers Azerbaijan’s ability to profit from Russia’s geopolitical distractions. Moreover, there is a heightened risk of instability in Azerbaijan and, more generally, in the region from the slump in oil. Colombia: Most people associate Venezuela as being a petroleum state, but its neighbor Colombia depends on oil as well, though to a much lesser extent. As a first order impact, we estimate that the decline in oil prices will cost Colombia 3%-4% of GDP in 2015 but the good news is that, unlike most oil producers, Colombia has a free floating exchange rate. The Colombian Peso has already fallen by about 25% versus US Dollar since it peaked in July 2014. This decline will help buffer Colombia’s highly diverse economy from the impact of lower oil prices. (Please see our Latin American Economic Outlook Article for more details). Iran: Although treated with suspicion by the West and under sanctions from many potential trading partners, Iran has a more diverse and less oil-reliant economy than most people might think. The decline in oil prices will shave about 6% off GDP in 2015 as a first order impact. Given Iran’s long-term economic decline, which began with the revolution in 1979 and was exacerbated by the war with Iraq (1980-1988), any further injury to the economy is unwelcome, but the country’s threshold for pain is quite high. While a GDP hit of 6% is fairly modest, Iran’s Achilles’ heel is likely to be its low level of currency reserves, which amount to only 26% of GDP and might be difficult to access given the international sanctions. One of Saudi Arabia’s goals in keeping oil prices low might be to force Iran to take more seriously negotiations with the West over its nuclear ambitions. The decline in oil prices is unlikely to create instability in Iran but it will likely constrain Tehran’s ability to influence outcomes in the region, to the delight of the Saudis and their allies. Iraq: Nowhere is the threat of instability caused by lower oil prices more apparent than in Iraq. The government relies on oil revenues for about 95% of its budget and has, at best, tenuous control of the areas outside of Baghdad and the South. Moreover, Iraq hasn’t had time to build up enormous currency reserves or a SWF to cushion the blow. Thus, the collapse of oil prices will vastly complicate the task of Haider al-Abadi’s government to fight ISIS and other militant groups that prevent it from taking control of parts of Northern and Western Iraq. The only silver lining here is that the collapse in oil prices will also deprive ISIS of a source of revenue. Instability in Iraq has the potential to create significant upside risk to oil prices, generally, and the Brent-WTI spread, in particular. Kazakhstan: The drop in oil prices is likely to shave about 10% off GDP in 2015 as a first order effect, but the actual impact could be deeper. Many Kazakh émigrés in Russia send back remittances. As such, the fall in oil prices and the related collapse in the Russian Ruble might also diminish this source of income and create tensions between Almaty and Moscow. The good news is that Kazakhstan has developed two SWFs with about $155 billion in combined assets, in addition to the nation’s $29 billion in currency reserves. This isn’t a huge cushion but should be enough to maintain stability for at least a few years before the impact of lower prices become fully apparent. One wild card: Kazakh President Nursultan Nazarbayev has called for early elections on April 26 and he has not yet declared his candidacy, although he is widely expected to do so. Kuwait: Lower oil prices could shave as much as 22.5% off Kuwait’s GDP as a first order impact but the good news is that the country has amassed among the largest currency and SWF reserves on the planet (as a percentage of GDP) and appears well positioned to weather the storm of lower oil prices for many years (perhaps as long as a decade), if need be. That doesn’t mean the pinch won’t be felt at all, just not to the point of causing near-term domestic instability. Libya: With oil prices likely to take off more than 25% from Libyan GDP, it would be tempting to say that the collapse in oil might foment instability. The problem is that Libya is already so unstable that it’s hard to imagine the situation getting materially worse. If anything, lower oil prices might paradoxically make the country more stable by reducing the intensity of the fighting over Libya’s oil assets. That said, Libya’s crude production could potentially decline, and if that occurs it risks re-inflating the Brent-WTI spread. Nigeria: Africa’s most populous nation is likely to see a first order GDP decline by about 7% as a result of the drop in oil prices. While some of the impact will be absorbed by a weaker currency and higher inflation, the hit to GDP is coming at an inopportune time. President Goodluck Jonathan has delayed Nigeria’s closely contested Presidential election until late March due to security concerns related to the Boko Haram militant group. Moreover, there has been long running instability in the oil producing delta region. Lower oil prices combined with Nigeria’s meager currency reserves could heighten the risk of instability that could curtail oil output and potentially boost the global price of oil as well as the Brent-WTI spread. Norway: The world’s wealthiest nation per capita will hardly notice the -5% first order GDP impact of lower oil prices because it will translate mainly to a smaller government surplus. Norway has almost no public debt and has massive currency reserves and a SWF with enough money to fund the entire GDP for over a year. If any country deserves a AAA rating, it’s Norway - oil price decline or not. Additionally, the Norwegian Krone has weakened modestly versus the Euro and more noticeably against the US Dollar, which will further insulate Norway from any negative impact from lower oil prices. Oman: This quiet neighbor of Saudi Arabia, the UAE and Yemen gets little attention but will take a huge hit to GDP (-16% first order impact) from the decline in oil prices. Moreover, unlike its Gulf neighbors, it has not amassed particularly large currency reserves nor does it have a big SWF to bail it out. Oman has been a paragon of domestic stability compared to neighboring Yemen but there is some risk that the problems in Yemen will spill across the border. We would recommend watching Oman closely during the next few years for any signs of trouble. Qatar: As a first order impact, the price of oil is likely to shave about 15% off Qatari GDP in 2015 but the actual impact will be much smaller. Qatar, like its peers in the Gulf, has amassed enormous currency and SWF reserves which total about 150% of GDP. This should allow Qatar to endure lower oil prices for a considerable period of time but it does bear mentioning that Qatar’s reserves are smaller than those of the Emiratis, Kuwaitis and Saudis relative to the size of its economy. While the Qataris can deficit spend for a while to blunt the impact of lower oil prices, the slowdown in petrol-related investment will at best slow the rate of economic growth with some risk of a near term recession. Russia: Since oil prices began falling in earnest in late 2014, the Western press has focused intensely on the impact that decline will have on Russia. We estimate a fairly modest hit of about 6% to GDP, which is closely in line with what Russia’s central bank and government estimate. Some of this will be offset by the Ruble’s decline (Figure 5), which will insulate Russian domestic industries from competitive imports and make Russian exports more competitive. It will also, of course, have the unwelcome effect of boosting Russia’s rate of inflation (Figure 6). Figure 5.

Figure 6.

Instability Influences Oil Supply and Prices, Which in Turn Influences Stability That said, Russia has a high threshold for pain after many years of crisis in the 1990s and, thus far, those hoping that lower oil prices would force Putin to back down on his support for Russian-speaking rebels in Ukraine have mostly been disappointed. He has reportedly narrowed his circle of advisors and focused on security hawks to the exclusion of more pro-Western voices among Russia’s billionaire class. Lower oil prices and the collapse of the Ruble have not been without consequence, however. Formerly staunch allies such as Belorussia and Kazakhstan are distancing themselves from Moscow, deepening Putin’s isolation. If anything, the collapse of oil prices may cause Putin and his inner circle to double down on their support for rebels in Ukraine, increasing the likelihood of conflict in the region. Russia’s foreign exchange reserves and other funds are relatively small compared to GDP, and its Forex reserves have been diminishing rather rapidly (Figure 7). Moreover, some of its private sector firms have debts denominated in Dollars and Euros that have suddenly become costlier to service with lower oil prices and the collapse on the Ruble. The situation in Russia isn’t all negative. The country has very little public sector debt (9% of GDP) and private sector debt is also reasonably low. Even so, with short-term interest rates at 15%, any debt will be expensive to service or to roll over. Figure 7.

Saudi Arabia: In 1986, the Saudis and the United States collaborated closely to lower oil prices to the detriment of Iran and the Soviet Union. Once again, the Saudi’s appear to be trying to kill many birds with one stone. We count at least four: ISIS (the Islamic State earns some revenue by siphoning off and selling oil); Iran (nuclear negotiations and other geopolitical matters); Russia (long-term support for pan-Arabists including Assad); and frackers in the United States. In fact, even more important than frackers in the United States are potential frackers elsewhere in the world. The Saudis can afford to refuse requests from other OPEC countries to curtail production and boost prices and, they appear willing to play the waiting game -- their currency and SWF assets add up to around 200% of GDP, making the -19.5% first order hit to GDP easily affordable for years to come. Moreover, the Kingdom has little debt. While it has been undergoing a delicate leadership transition, the Saudi state appears to have the resources to maintain stability for half a decade or more in the event that oil prices stay low. That said, if oil prices were to stay low indefinitely, security risks to the Kingdom would increase. These security risks include possible problems with the Shiites on the Gulf coast as well as with Sunni extremists and divisions within the increasingly large and complicated royal family. Finally, the Saudi oil company ARAMCO is already cutting costs, including a 25% cut to exploration and is also squeezing suppliers. This will likely slow the pace of growth of the Saudi economy and introduce some near-term risk of a downturn. United Arab Emirates: Like Kuwait and Saudi Arabia, the UAE is also well insulated from the drop in crude oil prices. With the regional banking, entertainment and travel hubs of Abu Dhabi and Dubai, the UAE has a more diversified and less petroleum-dependent economy than many of its neighbors –at least at first glance. The first order impact of lower oil prices will likely be about -11% of UAE GDP. This is fairly small compared to the Emiratis massive currency and SWF reserves, which total 233% of GDP. This should permit the UAE to maintain stability for many years even if low oil prices persist. That said, if regional commerce slows as a result of lower oil prices then it might take some of the luster off Abu Dhabi and Dubai, which might grow at a significantly slower pace than they are accustomed to or even experience a recession. Venezuela: The oil price collapse is this South American nation’s biggest nightmare. Venezuela, which depends on oil for 96% of export revenue, is running a massive budget deficit of around 20% of GDP and has blown through most of its currency reserves. Shortages of basic necessities abound and even taking photos of long lines in shops is now illegal. President Nicolas Maduro has approval ratings in the 20s and his party is facing legislative elections in October. Paradoxically, Venezuela is one country where the drop in crude oil prices might cause consumers to have to pay more for gasoline if the government is forced to curtail subsidies. 2015 will be a very difficult year for Venezuela, where hyperinflation and a high chance for instability have the potential to disrupt production at state oil company PdVSA. To prevent instability the government has been taking increasing repressive measures including arresting opposition figures such as Caracas Mayor Antonio Ledezma. Venezuela’s woes are shifting Latin American politics in Washington’s direction. Already two recipients of Venezuela’s largesse, Bolivia and Cuba, are busy thawing relations with the United States in anticipation that they won’t be getting much support from Caracas going forward. Other beneficiaries of Venezuela’s efforts to expand its influence in the region, including Argentina and Ecuador, might also find themselves more dependent on the United States for their future growth prospects. Yemen: Here the GDP impact will be fairly minor (-1.4%) and like Libya there is little risk that the country will descend into chaos since it’s already there. The real risk is that the problems in Yemen will spread to neighboring Oman and Saudi Arabia. Consequences for Global Asset Markets With oil prices in the dumps, petro dollars aren’t going to stop flowing altogether but they will flow much more slowly from oil producing countries to oil consuming countries and in a few cases they might even flow in reverse. Money from the Gulf States, in particular, has found its way into almost every imaginable asset class from bonds to equities to real estate (notably in London and Paris). These flows risk slowing down considerably, possibly putting downward pressure on the higher end of real estate markets as well as depriving Western equity and bond markets of a (fairly minor) pillar of support. Given the benefits of lower oil prices to the rest of the world, however, we expect that equity markets (outside of the petroleum sector of course) might remain fairly well bid. To the extent that lower oil prices strengthen economic growth in the developed world, government bonds might suffer, however, as yields are already very low and the downward impact of lower oil prices on inflation will prove short lived. Currency markets have already been impacted by the fall in oil prices, contributing to sell offs in the Canadian Dollar, Brazilian Real, Colombia Peso, Mexican Peso, Norwegian Krone and the Russian Ruble. If instability in the oil producing nations emerges, it has the potential to push crude oil prices and these currencies higher. That said, if oil prices remain low or go lower, we would expect these currencies to continue to underperform those of the non-oil producing nations. Perhaps the more important financial consequence of lower oil prices could be greater volatility. The potential for geopolitical surprises is somewhat heightened by lower oil prices and the negative consequences that they might have for stability in key oil producing countries, notably Angola, Iraq, Libya, Nigeria and Venezuela. Disruptions to oil supply could ultimately create spikes in oil prices and strong reactions from global bond, currency and equity markets. All examples in this report are hypothetical interpretations of situations and are used for explanation purposes only. The views in this report reflect solely those of the authors and not necessarily those of CME Group or its affiliated institutions. This report and the information herein should not be considered investment advice or the results of actual market experience. 盈透交易员睿智中提供的内容(包括文章和评论)仅作为资讯用途。发布的内容并不代表盈透证券建议您或您的客户联系独立顾问或对冲基金以期获取其服务或投资其产品,也不代表建议您联系在盈透交易员睿智发布文章或向顾问、对冲基金投资的相关人士。在盈透交易员睿智中发布文章的顾问、对冲基金或其他分析师均独立于盈透证券,盈透证券不会对这些顾问、对冲基金或其他人士的过往或将来表现,或其提供的信息之准确性做出任何声明或担保。盈透证券不会进行“适宜性评估”来确保顾问、对冲基金或其他参与方的交易适合于您。 发布内容中提及的证券或其他金融产品并非适合所有投资者。发布的内容并未从您的投资目标、财务状况或需求出发,并不旨在向您推荐任何证券、金融产品或策略。进行投资或交易前,您应考虑该产品是否适合您的特定情况,如有需要,请咨询相关人士获取专业的建议。过往业绩并不代表将来表现。 盈透或其分支机构的雇员所发布的任何信息均基于公认的真实可信的信息。然而,盈透或其分支机构无法保证信息的完整性、准确性和适当性。盈透不对任何金融产品其过去或将来的表现作出任何声明或担保。交易员睿智中发布的文章并不代表盈透认为任何特定金融产品或交易策略适合您。 The analysis in this article is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IB to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

★美国盈透证券是全美营收交易量最大的 顶尖互联网混业券商 盈透证券集团(IBG LLC)拥有超过50亿美元的综合股本资产 ★单一账户 多币种 直接接入全球24个国家100+市场中心,实现股票、期权、期货、外汇、债券、ETF及价差合约的全球配置 ★美国盈透证券有限公司的客户证券账户受到证券投资人保护公司("SIPC")最高达50万美元(现金额度25万美元)的保护 ★超低手续费 不卖订单流 致力提供最佳执行价格 ●享受盈透低佣金 外盘开户请点击: https://www.ibkr.com.cn/mkt/?src=7h5&url=%2Finv%2Fcn%2Fmain.php%23open-account ●详细开户流程: http://www.7hcn.com/article/187153-1.html 美国期货及期货期权收费根据交易量阶梯式计算 盈透佣金0.25-0.85美元/手 美股佣金半美分/股 超低隔夜融资利息 1000万美元年化利息低至0.594% (按目前基准利率0.13%计算)

每股净美元改善定义: ((价格改善股票数目 * 价格改善数额) - (没有价格改善股票数目 * 没有改善数额)) = 总执行股票数目 交易审计集团(TAG)。根据TAG,比较期间行业 作为整体考虑。TAG关于美国股票的分析包括所有100股或上至10,000股的市场定单。美国期权的分析包括所有市场定单尺寸并包括基于IB的成本相加 定价结构的客户收到的交易所回扣。 TAG对传递到欧洲交易所的定单的分析包括在正常交易时段内的所有传递执行的定单,包括交易所上市的股票的所有市价单和可交易的限价单以及近于市价单的定 单(定单收到时的限价价格距报价在十分之一欧元以内),并按每个交易所的执行交易量加权计算。欧洲股票的交易所包括XETRA, EURONEXT, CHI-X, WIENER BORSE, TURQUOISE,LONDON以及NASDAQ OMX。 ★专业交易平台- 交易者工作站(TWS)、网络交易者及多种移动交易端选择,包括手机交易平台及iPad交易平台方便您随时随地把握市场走势并及时作出交易指令, 并提供API及FIX连接解决方案 ★投资人服务商市场 向财务顾问、基金经理及第三方服务商提供向全球投资人展示业绩并开展合作的免费平台 ★根据不同客户需求 支持多种账户类型 包括对冲基金、职业/非职业顾问、自营交易商及白标经纪商账户 根据巴伦周刊互联网券商评比,盈透证券从2002年至2016年连续15年被巴伦周刊(Barron's)评为低成本经纪商:2002 - 5星,2003 - 4.9星,2004 - 5星,2005 - 5星,2006 - 5星,2007 - 4.8星,2008 - 4.5星,2009 - 4.5星,2010 - 4.2星,2011 - 4.5星,2012 - 4.3星,2013 - 4.5星,2014 - 4.5星,2015 - 4.5星,2016 - 4.5星。在巴伦周刊(Barron's)2016年3月21日的年度最佳互联网券商评比 - “网络投资者的最大顾虑?移动安全”中,盈透证券荣获4.5星评级。评比的条件包括交易体验和技术,使用性,移动性,交易产品范围,研究手段,投资组合分析和报告,客户服务和教育,以及成本。Barron's是Dow Jones & Co. Inc的注册商标。

欲了解更多信息请关注美国盈透证券公众微信号 或登录美国盈透证券官方网站:www.ibkr.com.cn/7hcn 欲了解更多信息请美国盈透证券官方网站:www.ibkr.com.cn 或直接联系我们深入了解个人账户及机构账户的相关服务: +852 2156 7907 ●享受盈透低佣金 外盘开户请点击: https://www.ibkr.com.cn/mkt/?src=7h5&url=%2Finv%2Fcn%2Fmain.php%23open-account ●详细开户流程: http://www.7hcn.com/article/187153-1.html

责任编辑:叶晓丹 |

【免责声明】本文仅代表作者本人观点,与本网站无关。本网站对文中陈述、观点判断保持中立,不对所包含内容的准确性、可靠性或完整性提供任何明示或暗示的保证。请读者仅作参考,并请自行承担全部责任。

本网站凡是注明“来源:七禾网”的文章均为七禾网 www.7hcn.com版权所有,相关网站或媒体若要转载须经七禾网同意0571-88212938,并注明出处。若本网站相关内容涉及到其他媒体或公司的版权,请联系0571-88212938,我们将及时调整或删除。

首页广告.png)

七禾研究中心负责人:刘健伟/翁建平

电话:0571-88212938

Email:57124514@qq.com

七禾科技中心负责人:李贺/相升澳

电话:15068166275

Email:1573338006@qq.com

七禾产业中心负责人:果圆/王婷

电话:18258198313

七禾研究员:唐正璐/李烨

电话:0571-88212938

Email:7hcn@163.com

七禾财富管理中心

电话:13732204374(微信同号)

电话:18657157586(微信同号)

七禾网 |  沈良宏观 |  七禾调研 |  价值投资君 |  七禾网APP安卓&鸿蒙 |  七禾网APP苹果 |  七禾网投顾平台 |  傅海棠自媒体 |  沈良自媒体 |

© 七禾网 浙ICP备09012462号-1 浙公网安备 33010802010119号 增值电信业务经营许可证[浙B2-20110481] 广播电视节目制作经营许可证[浙字第05637号]