聚合智慧 | 升华财富

聚合智慧 | 升华财富

产业智库服务平台

产业智库服务平台

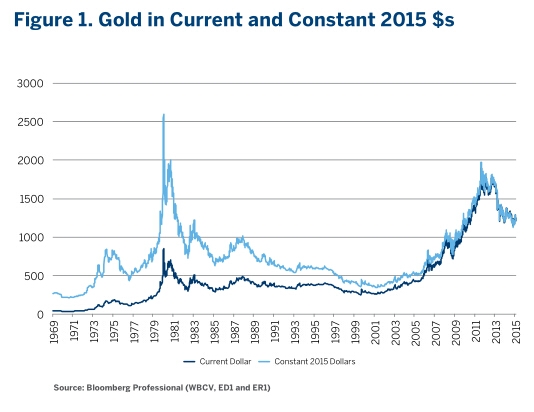

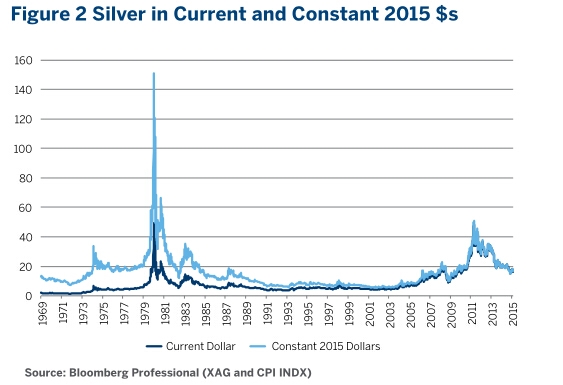

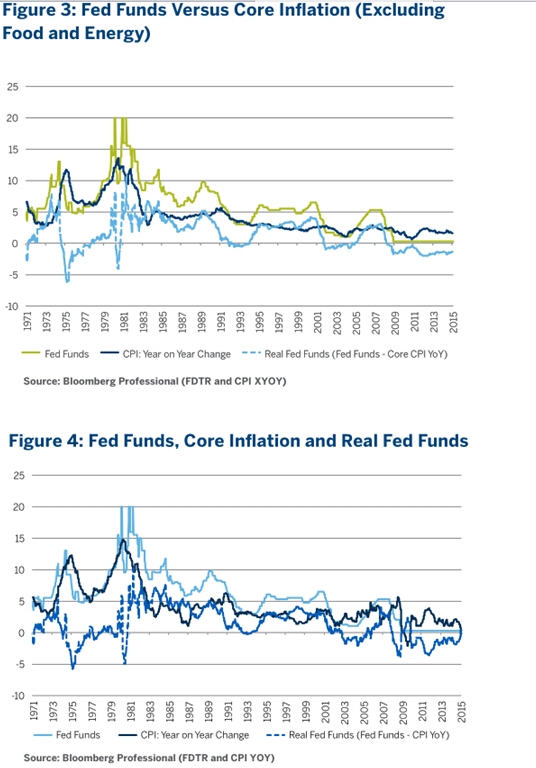

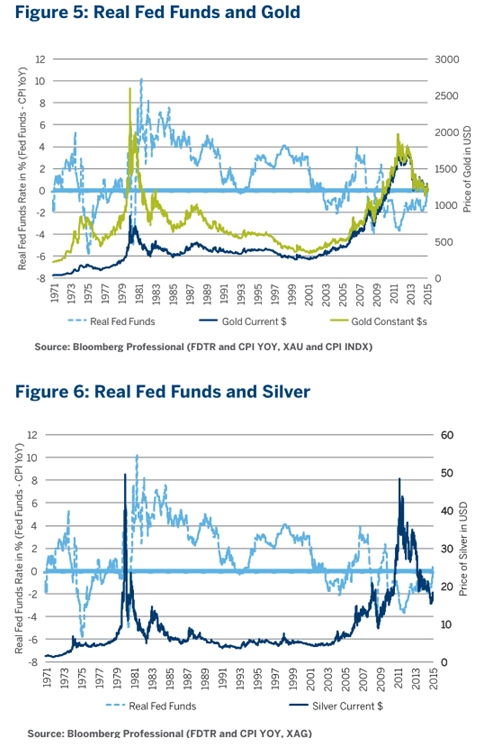

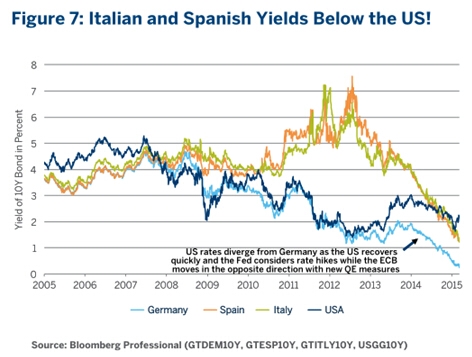

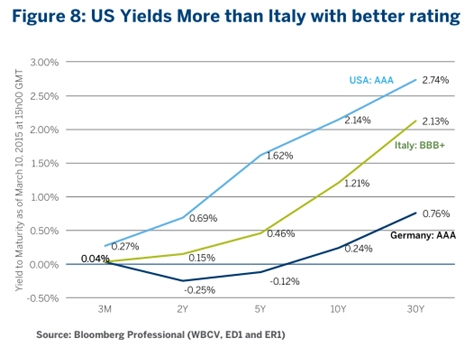

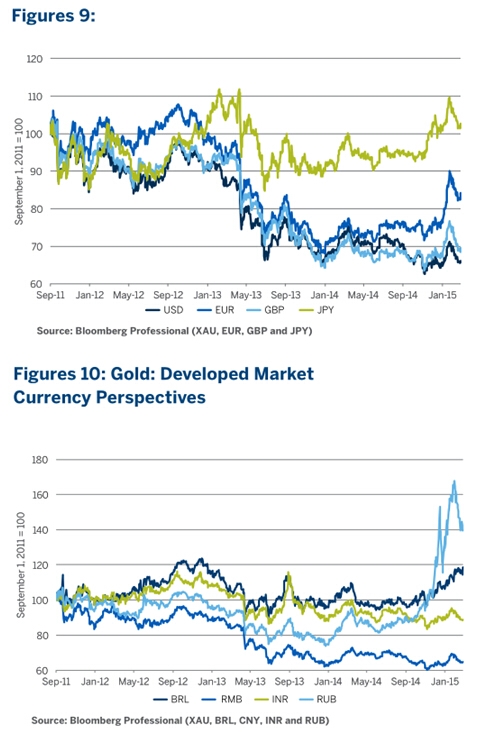

| Five Factors that Could Drive Gold and Silver… Lower or Higher! All examples in this report are hypothetical interpretations of situations and are used for explanation purposes only. The views in this report reflect solely those of the authors and not necessarily those of CME Group or its affiliated institutions. This report and the information herein should not be considered investment advice or the results of actual market experience. Gold and silver prices have fallen considerably from their 2011 highs. Silver peaked at nearly $50 per ounce and now trades below $20. Gold topped out at about $1,900 anounce and is currently close to $1,200. Both metals are not only trading far below their peaks, but also their inflation-adjusted highs set in 1980 (Figures 1 and 2). This gives asense of the scale of their downside and upside potential.  At least five factors may have contributed to their decline: 1) The steady recovery of the US economy has allowed the US Federal Reserve to end quantitative easing and begin considering rate hikes, possibly as soon as June. 2) The European Central Bank (ECB) has succeeded in containing the European debt crisis (at least excluding Greece) by promising to act as a buyer of last resort of the debt of Italy, Spain and other financially-challenged Eurozone countries, vastly reducing intra-European spreads. 3) The value of the US Dollar (USD), the currency of choice in the global commodities trade including gold and silver, has soared versus other currencies. 4) The prices of many other commodities including industrial metals, crude oil, natural gas and agricultural goods, have fallen in USD terms. 5) The crisis in the Middle East has not spread, at the moment, to the largest oil producing nations in the Persian Gulf. Let’s look at how gold and silver prices might trend basedon these possible drivers of market returns.  US Monetary Policy Since 2009, the Fed has found itself in the unusual position of holding its policy rate (Fed Funds) below the rate of core inflation. This is something that has only occurred on a few occasions (Figure 3). 1) 1969-1970: Rates were lowered to fight a mild recession. The Nixon Administration attempted to contain inflation afterwards with wage and price controls. 2) 1974-1977: When the Fed mistakenly thought that inflation from the first oil crisis would be temporary. This resulted in a massive run up in inflation from 1977-1980 that was reined in by soaring interest rates and a deep recession. 3) Brief periods of slightly negative real rates in 1992- 1993 and 2001-2004 when the economy was healing from recession.  When the Fed holds Fed Funds below the rate of headline inflation, there is a tendency for gold and silver prices to soar (Figures 5 and 6).  The tendency appears to last until the market begins to anticipate that the Fed will hike rates or tighten policy (by ending quantitative easing, for example). It is our view that the Fed is likely to begin tightening policy in 2015 for a variety of reasons: 1) A strong recovery in the labor market, with average hourly earnings up by 2.0% year- over-year and average hours worked increasing 0.6%. This makes for a 2.6% gain in average earnings, comparing February 2015 to February 2014 – quite respectable given the low rate of inflation. 2) The number of people working rose by 2.4% between February 2014 and February 2015. This brings the increase in total labor income to 5.0% (2.4% more people working + 2.6% increase in average wages). This should make for robust consumer spending. 3) The Fed sees the recent energy-related dip in inflation as being temporary. 4) Other areas of the economy appear to be robust, including corporate profits near a record high and the housing market continuing to recover slowly. As such, we would not be surprised if the Fed increases rates as soon as this June. Fed Funds futures reflect a rate hike by September and a second one by January 2016 – with the possibility that such rate moves could come sooner. If the Fed does raise rates as expected, it could pressure gold and silver prices. As such, we would not exclude the possibility of gold dipping below $1,000 per ounce into the triple digits, and silver making a run for below $10 per ounce. There are risks to this forecast, however. Equity markets have been trading at valuations that look reasonable so long as corporate earnings hold up. If corporate earnings begin to decline in 2015, however, there is a real possibility that the equity market could have its first major correction since 2011. Two previous Fed chairmen, Alan Greenspan and Ben Bernanke, were known for lowering interest rates (or ramping up quantitative easing) in the face of equity market weakness – dubbed the Greenspan and Bernanke puts. Will there be a put by current Fed Chair Janet Yellen as well? We don’t know, but it’s hard to imagine that she and the FOMC would risk exacerbating market volatility by hiking rates in the middle of a steep downturn in stocks. As such, if an equity market correction happens, to the extent that it delays Fed rate hikes, it might give at least a temporary boost to gold and silver prices. Bottom line, we think that US monetary policy holds more downside risks than upside potential for precious metals in 2015, but if the Fed delays rate hikes for any reason, it could be good for gold and silver. Europe While gold is denominated in US Dollars and therefore responds more strongly to changes in the Fed’s monetary policy than it does to actions by other central banks, the US isn’t the only game in town. On the other side of the Atlantic, it appears that the ECB’s gambit of promising to buy the debt of Italy, Spain and other financially-challenged Eurozone nations as a last resort has paid off.That promise, along with the announcement of a massive quantitative easing program, has pushed German yields close to zero, while Italian and Spanish yields have fallen below the yields on US Treasuries (Figure 7).  The easing of tensions in the Eurozone has been generally bad news for gold and silver. It eliminated the possibility of any imminent Eurozone break up to the disappointment of gold bugs who see the yellow metal as a store of value in times of inflation and uncertainty. The good news for investors in precious metals is that the process of calming the European rate markets is probably nearing an end. Simply put, rates might not be able to fall much further. German yields are already negative, below the six year point on the curve, and BBB+ rated Italian debt and BBB rated Spanish debt pay less than AAA (composite) rated debt in the United States. Once the ECB begins its buying program, there is a risk that rates might back up a bit. This won’t necessarily help gold and silver but the harm to gold and silver long position holders from the calming of the situation in Europe over the past few years is almost certainly over. Greece is the one exception. Its yields are still above 9% and Greece’s possible exit from the Eurozone monetary union, dubbed Grexit, could still happen later this year or in 2016. Even so, the impact of Greece’s withdrawal should be minor -- Europeans have already ring-fenced most of their private sector exposure to Greece, which constitutes less than 2% of the Eurozone economy. Bottom line: We see Eurozone events as a net neutral for gold and silver going forward.  US Dollar USD has soared against most other currencies in the past year for several reasons: 1) US economy is strengthening, as evidenced by a broad range of indicators. 2) That strength has allowed the Fed to end quantitative easing and has enabled the bank to seriously consider rate hikes in 2015. 3) Monetary policy is heading in the opposite direction in many other countries and regions, including the Eurozone where the ECB is embarking on a quantitative easing program: Japan, where the Bank of Japan continues to ease policy; and Australia and Canada where central banks have cut rates. 4) Commodity prices have collapsed, taking a diverse range of emerging market currencies down with them. Whether the current strength in the US Dollar will continue or not is difficult to say. Nevertheless, if it does keep its uptrend, it will likely put pressure on gold prices in USD terms but not necessarily from the perspective of buyers using other currencies (Figures 9 and 10).  Gold prices have fallen sharply since their September 2011 peaks in USD terms and from the perspective of other relatively strong currencies such as the British Pound (GDP) and Renminbi (RMB), but not from the perspective of weaker currencies such as Japanese Yen (JPY) or Russian Ruble (RUB) (Figures 9 & 10). This is a double-edged sword for gold and silver. On the one hand, from the standpoint of a buyer in India, Japan or Russia, gold has held its value from the perspective of their currency, which is desirable. On the other hand, from their vantage point, it has become more expensive to buy which could curtail their ability and willingness to purchase more of it in the future. Overall, the US Dollar rally might have some life left and if USD continues to power higher, it will be bad for gold. Any upside surprises on economic growth outside of the US or any downside shocks in the US could hurt the Dollar, however, and could boost the price of precious metals. Other Commodities Our base case view is that crude oil prices are unlikely to rebound towards $100 per barrel any time soon and that the most likely scenario is that prices could remain in a wide trading range from perhaps $30-$70 per barrel for the rest of 2015 and maybe even into 2016 and 2017. Most oil producers, whether they are indebted private sector companies or state entities serving government interests, are simply not in a position to cut back their current production which would result in a loss of revenue. For the moment, Saudi Arabia does not appear to be in the mood to cut back production. For the Saudis, lower oil prices are like killing several birds with one stone. Lower prices reduce investment in fracking in the US and elsewhere, which could boost prices several years down the road, although having little impact on current production. Lower prices also hinder Iran and Russia with which Saudi Arabia has contentious relations, and limit revenues of the Islamic State militant group. Industrial metals such as copper and aluminum have also weakened considerably. This appears to be related to slowing growth in China. We don’t see a change in this in 2015 and, in fact, expect China’s pace of growth to continue to moderate. Food prices are the hardest of all to predict since they are only modestly influenced by macroeconomic conditions and are subject to other forces such as weather. Geopolitics To the extent that the collapse in commodity prices can create political instability, notably in major oil producing nations, it could have upside benefits for gold and silver. Otherwise, we see the likelihood of continued low prices for other commodities in 2015 and 2016 as likely weighing on precious metals. (Please see our paper Oil Collapse: Winner and Losers, The Geopolitical and Economic Consequences of Lower Oil Prices). Overall, we see downside risks to gold and silver outweighing upside risks in 2015. That said, we think that the key upside risks to watch for are: 1) A US equity correction or slowdown in the US economy that causes the Fed to delay rate hikes or, in an extreme case, even to ease further. 2) Geopolitical instability, especially in the Middle East or other key oil producing nations. 3) A drop in the US Dollar. 4) Renewed questions about the viability of the Eurozone. Bottom line: We see Eurozone events as a net neutral for gold and silver going forward. 【附:盈透证券简介】  网开盈透做期货 佣金美刀两块多 股票期权和外汇 猛戳! ◆美国盈透证券是全美营收交易量最大的 顶尖混业互联网券商 ◆单一账户 多币种 直接接入全球24个国家100+市场中心,实现股票、期权、期货、外汇、债券、ETF及价差合约的全球配置 ◆超低手续费 美国期货及期货期权收费根据交易量阶梯式计算 盈透佣金0.25-0.85美元/手 ◆专业交易平台- 交易者工作站(TWS)、网络交易者及多种移动交易端选择,包括手机交易平台及iPad交易平台方便您随时随地把握市场走势并及时作出交易指令 ◆股东权益50亿美元 标普信用评级A- 展望稳定, 明显优于许多国际知名金融机构  ◆连续三年荣获美国主流专业投资期刊BARRON’S的最佳网络经纪商 》最适合期权交易者 》 最佳投资组合分析及报告 》最佳交易体验及交易技术 》 最低保证金借贷成本 》全球交易者最佳券商 》 10年连续最低成本券商 》频繁交易者最佳券商 》 最佳综合奖 ◆根据不同客户需求 支持多种账户类型 包括对冲基金、职业/非职业顾问、自营交易商及白标经纪商账户 欲了解更多信息请美国盈透证券官方网站:www.ibkr.com.cn/7hcn 或直接联系销售经理边嘉茵深入了解个人账户及机构账户的相关服务: 有【设立境外基金产品】需求的朋友也可以和边嘉茵联系: 手机:l39ll47336O 邮件: abian(a)ibkr.com 电话:+852 2156 79l5 美国盈透证券有限公司是 NYSE-FINRA-SIPC成员,并受美国证券交易委员会(SEC)和商品期货交易委员会(CFTC)监管 责任编辑:叶晓丹 |

【免责声明】本文仅代表作者本人观点,与本网站无关。本网站对文中陈述、观点判断保持中立,不对所包含内容的准确性、可靠性或完整性提供任何明示或暗示的保证。请读者仅作参考,并请自行承担全部责任。

本网站凡是注明“来源:七禾网”的文章均为七禾网 www.7hcn.com版权所有,相关网站或媒体若要转载须经七禾网同意0571-88212938,并注明出处。若本网站相关内容涉及到其他媒体或公司的版权,请联系0571-88212938,我们将及时调整或删除。

首页广告.png)

七禾研究中心负责人:刘健伟/翁建平

电话:0571-88212938

Email:57124514@qq.com

七禾科技中心负责人:李贺/相升澳

电话:15068166275

Email:1573338006@qq.com

七禾产业中心负责人:果圆/王婷

电话:18258198313

七禾研究员:唐正璐/李烨

电话:0571-88212938

Email:7hcn@163.com

七禾财富管理中心

电话:13732204374(微信同号)

电话:18657157586(微信同号)

七禾网 |  沈良宏观 |  七禾调研 |  价值投资君 |  七禾网APP安卓&鸿蒙 |  七禾网APP苹果 |  七禾网投顾平台 |  傅海棠自媒体 |  沈良自媒体 |

© 七禾网 浙ICP备09012462号-1 浙公网安备 33010802010119号 增值电信业务经营许可证[浙B2-20110481] 广播电视节目制作经营许可证[浙字第05637号]